Financial education is a crucial life skill that empowers individuals to make informed and effective decisions about their money. It encompasses knowledge, skills, and habits related to earning, saving, investing, and managing finances. With the growing complexity of the financial landscape, understanding financial education is no longer optional—it is essential for achieving financial stability and success.

This comprehensive guide explores everything you need to know about financial education, from its definition and importance to practical ways to improve your financial literacy. We will also answer seven frequently asked questions (FAQs) and conclude with actionable key takeaways.

Key Takeaways

- Definition: Financial education is the process of learning how to manage money effectively.

- Importance: It empowers individuals to make informed decisions, achieve financial freedom, and avoid financial pitfalls.

- Core Areas: Budgeting, saving, investing, debt management, and retirement planning are key components.

- Steps to Improve: Read books, take courses, use financial tools, and stay updated.

- FAQs Addressed: Common questions about financial literacy and its applications were covered to provide clarity.

What Is Financial Education?

Financial education refers to the process of acquiring knowledge and developing skills to effectively manage financial resources. It covers a wide range of topics, including budgeting, saving, investing, debt management, and understanding financial products such as loans, credit cards, and insurance.

In essence, financial education equips individuals with the tools they need to achieve financial goals, avoid financial pitfalls, and navigate life’s financial challenges with confidence.

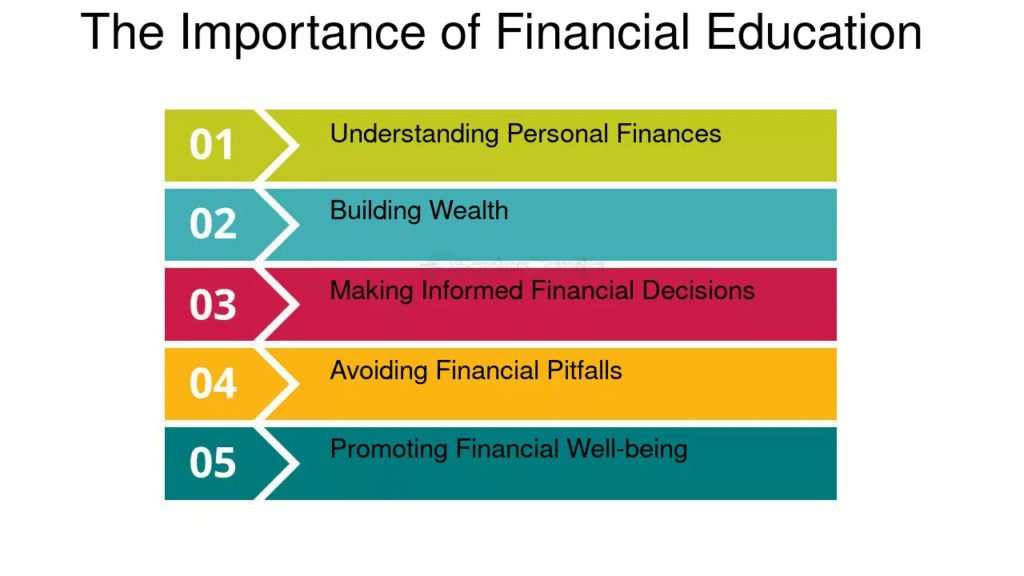

Why Is Financial Education Important?

Financial education is important because it empowers individuals to:

- Make Informed Decisions: Understanding financial concepts allows people to make smarter choices regarding spending, saving, and investing.

- Avoid Debt Traps: Knowledge of financial management helps individuals avoid excessive debt and high-interest loans.

- Achieve Financial Freedom: Financial literacy enables individuals to build wealth and attain financial independence.

- Prepare for Emergencies: By learning to save and invest wisely, people can prepare for unexpected expenses or economic downturns.

- Plan for the Future: Financial education supports long-term goals such as buying a home, funding education, or retiring comfortably.

Core Components of Financial Education

Financial education covers several key areas that are essential for effective money management:

1. Budgeting

Budgeting is the foundation of financial education. It involves creating a plan to allocate income toward expenses, savings, and investments. A well-structured budget helps individuals track their spending and avoid unnecessary expenses.

2. Saving

Saving involves setting aside a portion of income for future needs or emergencies. Financial education teaches strategies to save consistently and grow savings over time.

3. Investing

Investing is the process of using money to generate returns through assets like stocks, bonds, real estate, or mutual funds. Financial literacy helps individuals understand risk, diversify investments, and make informed investment decisions.

4. Debt Management

Debt management involves understanding how to use credit responsibly, pay off loans, and avoid falling into a debt cycle. This includes learning about interest rates, credit scores, and repayment plans.

5. Understanding Financial Products

Financial education includes knowledge of financial products such as savings accounts, credit cards, insurance policies, and retirement accounts. This helps individuals choose the right products for their needs.

6. Retirement Planning

Planning for retirement ensures financial security during later years. This includes learning about pensions, retirement savings accounts, and investment strategies to build a retirement corpus.

7. Tax Planning

Understanding taxes helps individuals minimize their tax liability through deductions, credits, and efficient financial planning.

Benefits of Financial Education

- Reduces Financial Stress: Managing money effectively reduces stress and anxiety related to financial uncertainties.

- Improves Quality of Life: Financial literacy supports a better standard of living by enabling individuals to meet their needs and pursue their goals.

- Promotes Economic Stability: At a macro level, financial education contributes to a stable economy by reducing default rates and promoting responsible financial behavior.

- Encourages Wealth Building: Financially educated individuals are more likely to invest and grow their wealth over time.

- Enhances Decision-Making Skills: With financial knowledge, people can confidently evaluate financial opportunities and risks.

How to Improve Financial Education

Improving your financial literacy is a continuous process. Here are practical steps to get started:

1. Read Books and Articles

Explore books like Rich Dad Poor Dad by Robert Kiyosaki or The Total Money Makeover by Dave Ramsey. Online articles and blogs are also valuable resources.

2. Take Online Courses

Platforms like Coursera, Udemy, and Khan Academy offer courses on personal finance and financial literacy.

3. Follow Financial Experts

Learn from financial advisors and experts who share insights through blogs, podcasts, or social media.

4. Use Financial Tools

Apps like Mint, YNAB (You Need a Budget), and Acorns help manage budgets, track expenses, and invest.

5. Practice Money Management

Apply what you learn by creating budgets, tracking expenses, and setting financial goals.

6. Stay Updated

The financial world is constantly changing. Keep up with trends, new financial products, and economic developments.

Emergency Fund Management

An emergency fund is crucial to ensuring financial stability during unexpected situations like job loss, medical emergencies, or urgent home repairs. Financial education can help individuals understand the importance of saving at least three to six months’ worth of living expenses in a liquid, easily accessible account.

Key Steps for Building an Emergency Fund:

- Set a monthly savings target.

- Open a high-yield savings account or money market account.

- Ensure the fund is separate from regular savings or investment accounts.

Credit Scores and Credit Reports

Understanding your credit score and how it impacts your financial life is essential. A high credit score can result in lower interest rates for loans, while a low score can make borrowing expensive or even impossible.

Key Factors Affecting Your Credit Score:

- Payment History (35%): Timely payments help improve your score.

- Credit Utilization (30%): Using less than 30% of your credit limit is ideal.

- Length of Credit History (15%): A longer credit history boosts your score.

- Types of Credit Used (10%): A mix of credit accounts is favorable.

- New Credit (10%): Opening too many new accounts in a short period may lower your score.

How to Improve Your Credit Score:

- Pay bills on time.

- Keep credit card balances low.

- Avoid opening too many new accounts.

- Regularly check your credit report for errors.

Investing in Real Estate

Real estate is often considered a reliable investment that can build wealth over time. Understanding the different types of real estate investments (residential, commercial, REITs, etc.) and the associated risks and returns is important for long-term wealth building.

Types of Real Estate Investments:

- Direct Ownership: Buying physical property to rent or sell.

- Real Estate Investment Trusts (REITs): A way to invest in real estate without owning physical properties.

- Crowdfunding: Pooling money with other investors to buy properties or invest in development projects.

Factors to Consider Before Investing in Real Estate:

- Location and market trends.

- Financing options and interest rates.

- Property management costs.

- Potential rental income or resale value.

Risk Management and Insurance

Insurance is a key component of financial education, as it helps mitigate risks. From health insurance to life insurance, understanding the different types and choosing the right policies based on personal needs is crucial for financial protection.

Common Types of Insurance:

- Health Insurance: Covers medical expenses.

- Life Insurance: Provides financial security to dependents in case of death.

- Disability Insurance: Replaces income if you’re unable to work due to illness or injury.

- Homeowners/Renters Insurance: Protects your property and belongings.

- Auto Insurance: Covers damage to vehicles or injury in an accident.

Tips for Choosing the Right Insurance:

- Assess the level of coverage you need.

- Compare policies to find the best rates.

- Review your coverage annually to ensure it still meets your needs.

Tax Planning and Optimization

Understanding taxes is vital for minimizing liabilities and optimizing deductions. Financial education in tax planning can help individuals reduce their taxable income, avoid penalties, and take advantage of available tax credits.

Key Tax Strategies:

- Tax-Deferred Accounts: Contribute to accounts like IRAs or 401(k)s to reduce your taxable income.

- Tax Credits vs. Tax Deductions: Understand the difference and choose the best option to reduce tax liability.

- Capital Gains: Be aware of tax rates on long-term vs. short-term capital gains.

Popular Tax-Advantaged Accounts:

- Retirement Accounts: 401(k), IRA, Roth IRA.

- Health Savings Accounts (HSAs): Tax-free savings for medical expenses.

- 529 Plans: Tax-free college savings plans.

Behavioral Finance

Behavioral finance studies the psychological influences on people’s financial decisions. It explains why individuals might make irrational financial choices, like emotional spending or avoiding investments out of fear.

Common Biases in Behavioral Finance:

- Loss Aversion: The tendency to fear losses more than the desire for gains.

- Anchoring: Relying heavily on initial information when making financial decisions.

- Overconfidence: Believing you know more than you do, which can lead to poor investment decisions.

How to Overcome Behavioral Biases:

- Be aware of emotional influences on financial decisions.

- Automate savings and investments to remove impulsivity.

- Use data and analysis rather than gut feelings for financial decisions.

Estate Planning

Estate planning ensures that your assets are distributed according to your wishes after death. Financial education in estate planning can help individuals understand the importance of wills, trusts, and powers of attorney.

Key Elements of Estate Planning:

- Wills: A legal document outlining how your assets will be distributed after your death.

- Trusts: A way to manage your assets during and after your lifetime, which can avoid probate.

- Powers of Attorney: Designating someone to manage your finances or healthcare decisions if you’re unable to do so.

Benefits of Estate Planning:

- Ensures that your wishes are honored after your death.

- Minimizes estate taxes and avoids probate.

- Provides clarity and financial security for your loved ones.

Understanding Cryptocurrencies

Cryptocurrency is a rapidly growing asset class that is still evolving. Understanding how cryptocurrencies work, including risks, regulations, and potential rewards, is crucial for anyone considering investing in this space.

Key Concepts in Cryptocurrencies:

- Blockchain: The decentralized technology that underpins cryptocurrencies.

- Bitcoin and Altcoins: The difference between Bitcoin (the first cryptocurrency) and other cryptocurrencies like Ethereum, Litecoin, etc.

- Wallets and Exchanges: Platforms to store and trade cryptocurrencies.

Risks to Consider:

- Volatility: Cryptocurrencies can experience sharp price fluctuations.

- Security: Hacking risks and theft of digital assets.

- Regulation: Cryptocurrency laws and regulations vary by country and may change over time.

Financial Planning for Small Businesses

For entrepreneurs, managing business finances is crucial for success. Financial education for small business owners covers areas like budgeting, cash flow management, and business taxes.

Key Aspects of Small Business Financial Education:

- Cash Flow Management: Ensuring that the business has enough liquidity to meet operational needs.

- Profit and Loss Statements: Analyzing business profitability.

- Tax Considerations: Understanding business tax obligations and potential deductions.

- Debt Financing vs. Equity Financing: Choosing between loans or selling ownership stakes to fund business growth.

Social Security and Pension Planning

Understanding social security benefits and pension planning is critical for those nearing retirement. Financial education in this area helps individuals optimize their retirement income streams.

Important Concepts:

- Social Security Benefits: How to maximize benefits by considering when to start taking them.

- Pensions and Annuities: How employer-sponsored pension plans or annuities can provide steady income in retirement.

Financial Independence and Early Retirement (FIRE Movement)

The Financial Independence, Retire Early (FIRE) movement has gained popularity in recent years. It’s about aggressively saving and investing a significant portion of your income to achieve financial independence at an early age—often in your 30s or 40s—allowing you to retire long before the typical retirement age of 65.

Key Concepts of the FIRE Movement:

- Financial Independence (FI): Reaching a point where your investments or passive income cover all your living expenses, allowing you to live without relying on a job.

- Early Retirement (RE): The freedom to leave your job and focus on passions, hobbies, or volunteering, knowing that you have sufficient income from investments.

- Extreme Savings Rate: Many FIRE followers aim to save 50% to 75% of their income, cutting unnecessary expenses and focusing on maximizing savings and investments.

How to Achieve FIRE:

- Increase Income: To save aggressively, many FIRE adherents increase their income by taking on higher-paying jobs, side hustles, or freelance work.

- Reduce Expenses: The goal is to live below your means, which often involves drastic lifestyle changes, like downsizing housing, cutting discretionary spending, or using public transport instead of owning a car.

- Invest Wisely: The bulk of the savings is invested in low-cost, diversified index funds or other growth assets that generate returns over time.

- 4% Rule: A common rule of thumb in the FIRE movement is the “4% Rule,” which suggests that you can safely withdraw 4% of your investment portfolio each year in retirement without running out of money. To retire early, you would aim to accumulate 25 times your annual living expenses in investments.

Pros of the FIRE Movement:

- Freedom: You have the flexibility to retire early and focus on things that bring you joy and purpose.

- Financial Security: By aggressively saving and investing, you build a solid financial foundation that helps you avoid debt and financial uncertainty.

Challenges and Criticisms:

- Lifestyle Sacrifices: The extreme savings rate may require significant lifestyle changes, which might not be appealing to everyone.

- Longevity Risk: Retiring early means relying on your investments for potentially decades, and there’s the risk of outliving your money if markets underperform or withdrawals are mismanaged.

- Health Insurance: In some countries, like the U.S., health insurance is tied to employment, so retiring early could require securing expensive coverage until Medicare kicks in at age 65.

The Psychology of Money: Understanding Your Money Mindset

The way we think about money—our money mindset—greatly influences our financial decisions and behaviors. The psychology of money explores how emotions, biases, and beliefs shape our financial habits and choices.

Key Money Mindsets:

- Abundance vs. Scarcity Mindset:

- Abundance Mindset: Believing that there is enough wealth for everyone and that opportunities are abundant. People with an abundance mindset tend to be more open to investment opportunities and are confident in their ability to earn more money.

- Scarcity Mindset: Focusing on lack or limitation, believing that there is never enough money. This mindset can lead to hoarding, fear-based financial decisions, or missed opportunities for growth.

- Fixed vs. Growth Mindset:

- Fixed Mindset: Believing that your financial situation is fixed and unchangeable, which can lead to complacency or avoidance of learning new financial strategies.

- Growth Mindset: Viewing financial challenges as opportunities to learn and improve. Individuals with a growth mindset tend to be proactive about increasing their financial literacy, learning new investment strategies, and adapting to changing circumstances.

- Risk Tolerance: The amount of risk an individual is willing to take on in investments or financial decisions. This is often tied to personal experiences and attitudes toward financial security.

- High Risk Tolerance: Willing to invest in volatile assets or take risks in hopes of higher rewards.

- Low Risk Tolerance: Preferring safe, low-risk investments to protect wealth, even if the returns are lower.

Emotional Influences on Money Decisions:

- Fear: Fear of loss can lead to avoiding investments or selling off assets during market downturns, missing out on long-term growth.

- Guilt: Some people feel guilty about spending money on things they want, leading to excessive frugality or neglecting self-care.

- Greed: On the opposite side, greed can cause risky financial behaviors, such as chasing get-rich-quick schemes or over-leveraging investments.

Cognitive Biases that Affect Money Decisions:

- Anchoring Bias: Relying too heavily on initial information (such as the price of a stock or a real estate listing) and failing to adjust it as new information becomes available.

- Loss Aversion: The psychological tendency to fear losses more than valuing gains, which can lead people to hold onto losing investments for too long or avoid investments altogether.

- Confirmation Bias: Seeking information that supports pre-existing beliefs, leading to poor decision-making or ignoring valuable financial advice.

Developing a Healthy Money Mindset:

- Mindful Spending: Recognize your emotional triggers around spending, and practice being intentional about where your money goes.

- Positive Affirmations: Use affirmations to shift from a scarcity mindset to an abundance mindset, reinforcing the belief that you can create wealth and financial stability.

- Financial Therapy: In some cases, seeking the help of a financial therapist or counselor can be beneficial for addressing deep-rooted emotional issues around money.

- Focus on Long-Term Goals: Shift your focus from short-term gratification to long-term wealth building, aligning your daily choices with your broader financial goals.

Read More: Why Should Everyone Learn Financial Literacy?

Conclusion

Financial education is a vital skill for navigating today’s complex financial environment. It empowers individuals to make informed decisions, avoid financial pitfalls, and achieve their goals. By learning about budgeting, saving, investing, and managing debt, anyone can take control of their financial future.

Whether you are a student, professional, or retiree, improving your financial literacy is a lifelong process that pays dividends. Start small, stay consistent, and watch your financial confidence and stability grow.

FAQs

What is the difference between financial literacy and financial education?

Financial literacy refers to the ability to understand and apply financial concepts, while financial education is the process of learning those concepts.

Who needs financial education?

Everyone, regardless of age or income level, can benefit from financial education. It is especially important for students, young professionals, and small business owners.

How does financial education help students?

Financial education helps students manage student loans, budget their expenses, and develop good financial habits early in life.

What are some common financial mistakes to avoid?

Common mistakes include overspending, neglecting savings, taking on high-interest debt, and not investing for the future.

How can parents teach financial education to children?

Parents can teach children about money by giving allowances, encouraging savings, and explaining basic financial concepts like budgeting and spending.

Can financial education help with debt management?

Yes, financial education provides tools and strategies to reduce debt, manage repayments, and avoid future financial pitfalls.

Is financial education available in schools?

In many countries, financial education is being introduced in school curriculums. However, its availability varies by region and institution.